As we enter 2021, there has been a lot of talk regarding rising insurance premiums. The reality is that insurance premiums are a fact of life and many business owners are wondering how their premiums work and how can they reduce them.

In this guide, we’ll discuss all things insurance premiums from an broking professional, Brendan Goddard.

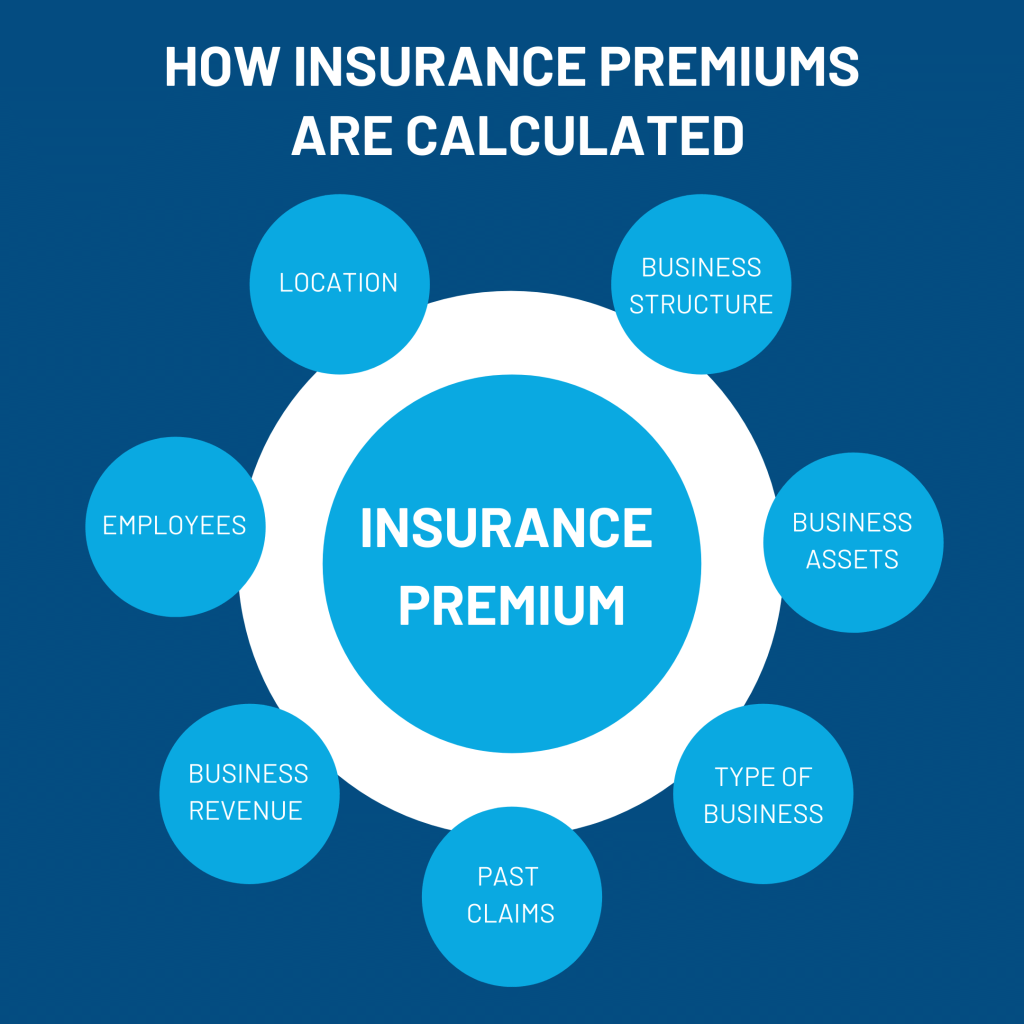

What is an insurance premium?

An insurance premium is a payment made in exchange for an insurance policy. This amount can be a once-off annual payment or sometimes broken down into smaller instalments such as monthly payments. In other words, it’s a contract made between yourself (or your business) with an insurer that guarantees financial help if you have become exposed to damage or loss agreed upon in the insurance contract.

How insurers calculate insurance premiums

When purchasing insurance, the insurer will take in several factors to calculate your premium. Insurers will evaluate what your likelihood of making a claim would be and consider the level of risks you’re exposed to, as well as the coverage amount.

It may be difficult to obtain insurance if insurers deem your risks being too high or the coverage amount is considerable.

When working with an insurance broker, they will make a general assessment of your risks and estimate coverage level. From there, they source quotes from insurers for an appropriate coverage amount.

Do premiums rise every year?

Although it may feel like premiums rise every year, it depends on factors both inside and outside of your control. Premiums may increase if your situation has changed or if you have an increase in exposure to risks than you had from the last renewal. However, the opposite can be true if you have made changes that reduce risks, resulting in lower premiums.

Premiums can also increase across the board, regardless of your circumstances. Inflation, increased claims, natural disasters and increased insurance operator costs can directly impact your insurance premium.

Brendan has seen how increased premiums have affected his clients.

“We are experiencing increases across all classes of insurance – from your business insurance through to your home insurance. Although this is a challenge for our clients, there are certain reasons why these increases are coming through.”

Will premiums rise in 2021?

Over the past twelve months, we have watched significant events take place locally and globally. From December 2019 to February 2020, Australia experienced some of the worst bushfires that devested entire states.

These bushfires caused an influx of claims and placed pressure on insurers to pay claims swiftly. Following the bushfires, the global COVID-19 pandemic caused a downturn in the economy, and again, insurers took another direct hit.

Even recently, Australia’s summer was the wettest in four years, with official data showing there was above average rainfall from the cooling La Niña – resulting in increased storm activities and insurance claims.

“The main issue is that the recent bushfires, coupled with natural weather events such as storms and also a pandemic, has lead insurers to paying out billions of dollars in claims. The unexpectedly high volume of claim payouts then directly hits the insurance companies balance sheets, placing them in a delicate position.”

Brendan then explains how COVID-19 has impacted the insurance industry and how it affects premium costs.

“Covid-19 is probably the biggest issue for insurance companies globally.”

“As businesses slowed down or ceased to operate, many no longer required insurance. With fewer insurance policies and less premiums collected, this resulted in a reduced pool of funds to help to pay for claims.”

“At the end of the day, rising premiums is a global issue, not just an Australian issue.”

2020 hasn’t been the best year for many. Despite insurance companies’ best efforts not to increase premiums, the money has to come from somewhere.

What to do if your insurance premiums have increased

Here at Macey Insurance Brokers, we have seen these premium increases passed onto our clients. However, Brendan and the team are proactively implementing ways to help reduce premiums.

“When it comes to renewals, we go through a process of analysing and researching the business, occupation, property or asset that we’re insuring. We review the risk profiles and then go to the marketplace and look at getting quotes with several different insurers that best suit that particular business.”

“From there, we look at the policy wordings from those insurers and then review to make sure the covers suits the business and then if we’ve got multiple insurers with the same policy conditions, then we look at the price.”

Brendan also recommends other ways of reducing your premiums in your business:

- Implement employee safety incentive programs

- Regularly evaluate safety policies and procedures

- Install security systems and CCTV

- Install fire sprinkler systems and other fire prevention equipment

- Improve infrastructures such as the installation of handrails

- Purchase safety equipment, such as pallet lifts, personal protective equipment and anti-slip mats

- Invest in advanced cybersecurity and IT infrastructures

Ultimately, as we have seen in the past, insurance premiums will continue to rise and fall. Having an insurance broker by your side can not only help you try to reduce your premiums but can be an advocate for your business.

If you would like to understand more about insurance premiums or would like assistance with your insurance, reach out to our friendly team, and we can take care of the rest.